Concept

Usage-based insurance (UBI), also known as pay as you drive (PAYD), pay how you drive (PHYD) and mile-based auto insurance, is a type of vehicle insurance whereby the costs are dependent upon type of vehicle used, measured against time, distance, behavior and place.

This differs from traditional insurance, which attempts to differentiate and reward “safe” drivers, giving them lower premiums and/or a no-claims bonus. However, conventional differentiation is a reflection of history rather than present patterns of behaviour. This means that it may take a long time before safer (or more reckless) patterns of driving and changes in lifestyle feed through into premiums.

![]()

Types

There are three types of usage-based insurance:

- Coverage is based on the odometer reading of the vehicle.

- Coverage is based on mileage aggregated from GPS data, or the number of minutes the vehicle is being used as recorded by a vehicle-independent module transmitting data via cellphone or RF technology.[3]

- Coverage is based on other data collected from the vehicle, including speed and time-of-day information, historic riskiness of the road, driving actions in addition to distance or time travelled.

The formula can be a simple function of the number of miles driven, or can vary according to the type of driving or the identity of the driver. Once the basic scheme is in place, it is possible to add further details, such as an extra risk premium if someone drives too long without a break, uses their mobile phone while driving, or travels at an excessive speed.

Telematic usage-based insurance (i.e. the latter two types, in which vehicle information is automatically transmitted to the system) Sinocastel OBD II provides a much more immediate feedback loop to the driver, by changing the cost of insurance dynamically with a change of risk. This means drivers have a stronger incentive to adopt safer practices. For example, if a commuter switches to public transport or to working at home, this immediately reduces the risk of rush hour accidents. With usage-based insurance, this reduction would be immediately reflected in the cost of car insurance for that month.

The smartphone as measurement probe for insurance telematics has been surveyed.

Usage-based Insurance(UBI) forms

Pay as you drive (PAYD) means that the insurance premium is calculated dynamically, typically according to the amount driven.

Another form of usage-based insurance is PHYD (Pay How You Drive). Similar to PAYD, but also brings in additional sensors like accelerometer to monitor driving behavior.

Potential benefits

- Social and environmental benefits from more responsible and less unnecessary driving.

- Commercial benefits to the insurance company from better alignment of insurance with actual risk. Improved customer segmentation.

- Potential cost-savings for responsible customers.

- Technology that powers UBI/PAYD enables other vehicle-to-infrastructure solutions including drive-through payments, emergency road assistance, etc.

- More choice for consumers on type of car insurance available to buy.

- Higher-risk drivers pay most per use, thus have highest incentive to change driving patterns or get off the roads, leaving roads more safe.

- For telematic usage-based insurance: Continuous tracking of vehicle location enhances both personal security and vehicle security. The GPS technology could be used to trace the vehicle whereabouts following an accident, breakdown or theft.

- The same GPS technology can often be used to provide other benefits to consumers, e.g. satellite navigation.

Usage-based Insurance Market Size

Increasing awareness regarding the advantages of UBI policies has created significant interest among consumers. For instance, according to an insurance telematics solution provider, a national driver survey found that around 70% of drivers in the UK expected to drive more miles in 2023 than the previous year. Moreover, around 58% stated that they would prefer to have a telematics insurance policy so that costs associated with increased mileage and car usage could be reduced. This is expected to encourage organizations to offer comprehensive solutions to customers and offer personalized programs based on their requirements and habits.

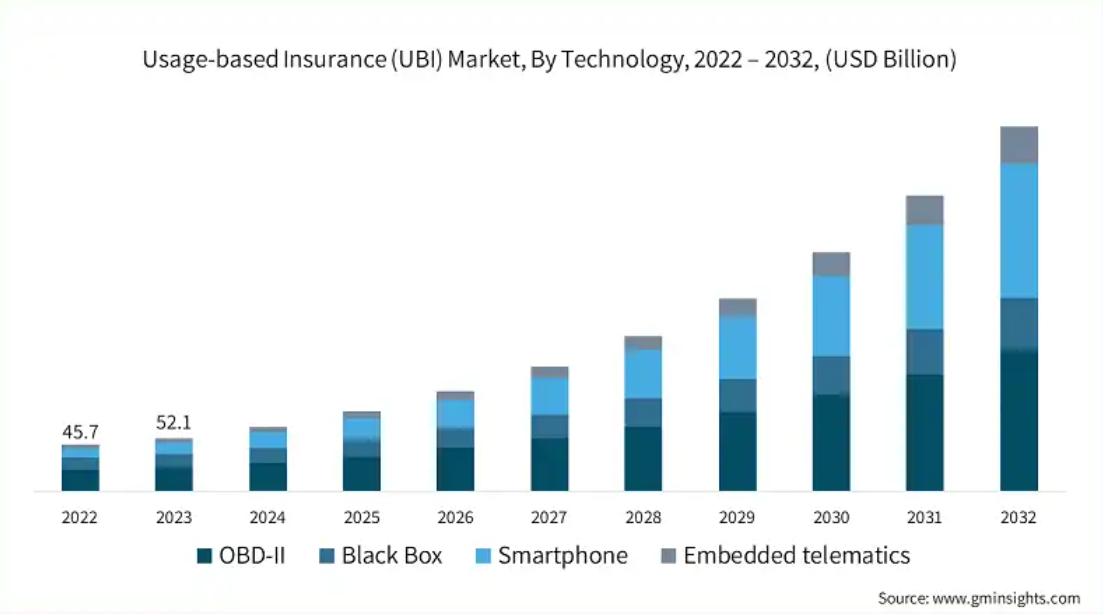

Usage-based Insurance Market size was valued at USD 52.1 billion in 2023 and is estimated to register a CAGR of over 24% between 2024 and 2032. Usage-based insurance, a type of auto insurance, utilizes in-vehicle communication systems to monitor mileage and driving habits. Telematics systems offer precise insights into driving patterns and safety practices, empowering insurers to adjust premiums in real time based on the perceived risk.

Usage-based Insurance Market Trends

Technological advancements are reshaping the landscape of usage-based insurance (UBI), influencing the way to assess risk and price policies among insurers. A key trend is the integration of advanced telematics systems, encompassing GPS and speed monitoring, directly into vehicles and mobile devices. These systems furnish real-time driving behavior data, enabling insurers to offer precise and current pricing.

The market is divided into OBD-II, Black Box, Smartphone, and Embedded telematics. In 2023, OBD-II(Sinocastel 218L) accounted for over 49% of the market share. Given the rising popularity of connected cars and the subsequent surge in driver data, telematics technology has become pivotal. It empowers insurance providers to tap into this wealth of information, covering driving patterns, maintenance needs, and overall vehicle performance.